It was not only UK share values that rose during 2016

Note: the Xafinity Transfer Value Index tracks the transfer value that would be provided by an example defined benefit pension scheme to a member aged 64 who is currently entitled to a pension of £10,000 each year starting at age 65 (and which increases each year in line with inflation). Different schemes calculate transfer values in different ways. A given individual may therefore receive a transfer value from their scheme that is significantly different from that shown.

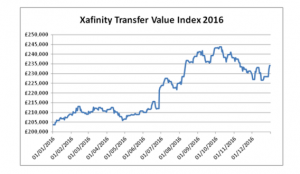

Transfer values from final salary pension schemes ended 2016 15% higher than where they started, according to Xafinity Consulting, a pension and employee benefit consultant. The increase was largely due to changes in long-term interest rates: as rates fall, so transfer values increase (and vice versa). Long-term rates dropped sharply in the wake of the Brexit vote, but then marginally backtracked in the final quarter – hence the slight decline in transfer values recorded by the Index.

However, as pension schemes often review their transfer value calculation basis on a regular cycle rather than reacting to every market move, some schemes have yet to take account fully of the most recent rate changes.

If you have final salary benefits from a previous employment, you might be lucky and find that your scheme is quoting transfer values still at or close to the peak levels of last October.

Even if the scheme’s calculation basis is more up to date, it could still be worth asking for a transfer value quotation. We can then use that figure, alongside a raft of other data, to assess whether the value is worth taking in your circumstances.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Article Posted: Feb 2017