Article posted: 8 April 2015

Pension tax: a post-election change – whoever wins

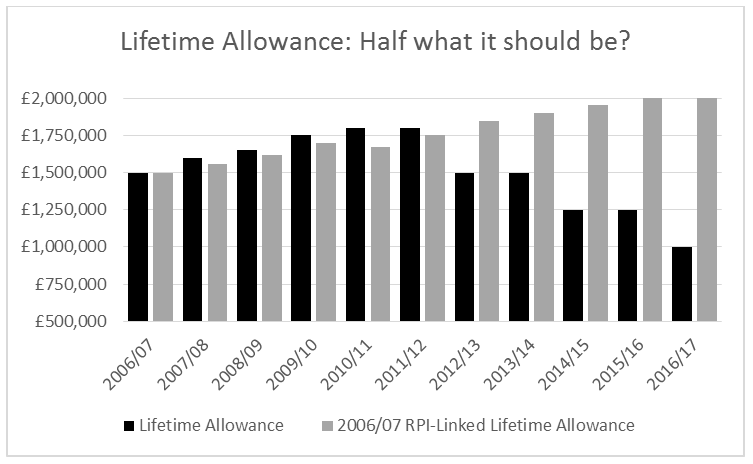

The lifetime allowance (LTA) is a key component of the pension tax rules. It effectively sets the normal maximum value of retirement/death benefits, beyond which a tax charge of up to 55% may apply. When the current ‘simplified’ (sic) pension tax rules started life in April 2006, the LTA was set at £1.5m, with increases to £1.8m scheduled through to 2010/11.

However, after 2010/11 there were no more LTA increases. Instead there were cuts in 2012 (to £1.5m) and 2014 (to the current £1.25m). The Chancellor announced a third LTA reduction in the Budget, taking the allowance down to £1m in 2016/17. Two years later, the LTA will become index-linked, albeit to the CPI rather than the RPI or earnings. As the graph below shows, had the original £1.5m had been RPI-linked from the start, by April 2016 it would have been around double the actual level.

There will be another set of transitional protection rules covering the cut, details of which are awaited. If your retirement funds are likely to be worth – or already are worth – over £1m, you will need to consider taking advantage of these.

Although the change is not legislated for in the Finance Act which has just received a rushed Royal Assent, there is little chance of the £1m limit not becoming a reality. The Shadow Chancellor, Ed Balls, announced in February just such a cut as part of a set of pension tax increases to finance a reduction in student tuition fees from £9,000 to £6,000 a year.

While £1m may sound more than adequate for a pension pot, considering current annuity rates, at age 65 it will only buy you an index linked pension of about £2,750 a month before tax. Therefore you may need to review your retirement planning…